pmdarima

Auto ARIMA

wangzf / 2022-11-12

安装及加载

依赖

- Numpy (>=1.17.3)

- SciPy (>=1.3.2)

- Scikit-learn (>=0.22)

- Pandas (>=0.19)

- Statsmodels (>=0.11)

PyPI

$ pip install pmdarima

Conda

$ conda config --add channels conda-forge

$ conda config --set channel_priority strict

$ conda install pmdarima

常规使用方式

import pmdarima as pm

from pmdarima.arima import auto_arima

API

import pmdarima as pm

arima

from pmdarima import arima

- ARIMA estimator & statistical tests

arima.ADFTestarima.ARIMAarima.AutoARIMAarima.CHTestarima.KPSSTestarima.OCSBTestarima.PPTestarima.StepwiseContext

- ARIMA auto-parameter selection

arima.auto_arima

- Differencing helpers

arima.is_constantarima.ndiffsarima.nsidffs

- Seasonal decomposition

arima.decompose

datasets

from pydarima import datasets

- Dataset loading functions

datasets.load_airpassengersdatasets.load_ausbeerdatasets.load_austresdatasets.load_gasolinedatasets.load_heartratedatasets.load_lynxdatasets.load_msftdatasets.load_sunspotsdatasets.load_taylordatasets.load_wineinddatasets.load_woolyrnq

metrics

from pmdarima import metrics

- Metrics

metrics.smape:对称平均绝对百分比误差

import numpy as np

y_true = np.array([0.07533, 0.07533, 0.07533, 0.07533, 0.07533, 0.07533, 0.0672, 0.0672])

y_pred = np.array([0.102, 0.107, 0.047, 0.1, 0.032, 0.047, 0.108, 0.089])

smape = metrics.smape(y_true, y_pred)

print(smape)

42.60306631890196

model_selection

from pydarima import model_selection

- Cross validation & split utilities

model_selection.RollingForecastCV([h, step, …])model_selection.SlidingWindowForecastCV([h, …])model_selection.check_cv([cv])model_selection.cross_validate(estimator, y)model_selection.cross_val_predict(estimator, y)model_selection.cross_val_score(estimator, y)model_selection.train_test_split(*arrays[, …])

pipeline

from pydarima.pipeline import Pipeline

- Pipelines

pipeline.Pipeline

preprocessing

from pydarima import preprocessing

- Endogenous transformers

preprocessing.BoxCoxEndogTransformerpreprocessing.LogEndogTransformer

- Exogenous transformers

preprocessing.DateFeaturizerpreprocessing.FourierFeaturizer

utils

from pydarima import utils

- Array helper functions & metaestimators

utils.acfutils.as_seriesutils.cutils.check_endogutils.diffutils.diff_invutils.if_has_delegateutils.is_iterableutils.pacf

- Plotting utilities & wrappers

utils.autocorr_plotutils.decomposed_plotutils.plot_acfutils.plot_pacf

快速开始

创建 Array

import pmdarima as pm

# array like vector in R

x = pm.c(1, 2, 3, 4, 5, 6, 7)

print(x)

[1 2 3 4 5 6 7]

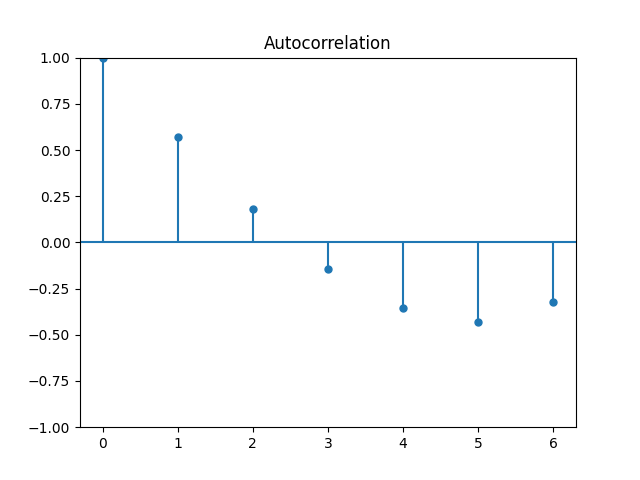

ACF 和 PACF

import pmdarima as pm

# acf

x_acf = pm.acf(x)

print(x_acf)

pm.plot_acf(x)

[ 1.0 0.57142857 0.17857143 -0.14285714 -0.35714286 -0.42857143 -0.32142857]

import pmdarima as pm

# pacf

x_pacf = pm.pacf(x)

print(x_pacf)

pm.plot_pacf(x)

Auto-ARIMA

载入依赖库

import numpy as np

from pmdarima.datasets import load_wineind

import pmdarima as pm

数据

# data

wineind = load_wineind().astype(np.float64)

wineind

array([15136., 16733., 20016., 17708., 18019., 19227., 22893., 23739.,

21133., 22591., 26786., 29740., 15028., 17977., 20008., 21354.,

19498., 22125., 25817., 28779., 20960., 22254., 27392., 29945.,

16933., 17892., 20533., 23569., 22417., 22084., 26580., 27454.,

24081., 23451., 28991., 31386., 16896., 20045., 23471., 21747.,

25621., 23859., 25500., 30998., 24475., 23145., 29701., 34365.,

17556., 22077., 25702., 22214., 26886., 23191., 27831., 35406.,

23195., 25110., 30009., 36242., 18450., 21845., 26488., 22394.,

28057., 25451., 24872., 33424., 24052., 28449., 33533., 37351.,

19969., 21701., 26249., 24493., 24603., 26485., 30723., 34569.,

26689., 26157., 32064., 38870., 21337., 19419., 23166., 28286.,

24570., 24001., 33151., 24878., 26804., 28967., 33311., 40226.,

20504., 23060., 23562., 27562., 23940., 24584., 34303., 25517.,

23494., 29095., 32903., 34379., 16991., 21109., 23740., 25552.,

21752., 20294., 29009., 25500., 24166., 26960., 31222., 38641.,

14672., 17543., 25453., 32683., 22449., 22316., 27595., 25451.,

25421., 25288., 32568., 35110., 16052., 22146., 21198., 19543.,

22084., 23816., 29961., 26773., 26635., 26972., 30207., 38687.,

16974., 21697., 24179., 23757., 25013., 24019., 30345., 24488.,

25156., 25650., 30923., 37240., 17466., 19463., 24352., 26805.,

25236., 24735., 29356., 31234., 22724., 28496., 32857., 37198.,

13652., 22784., 23565., 26323., 23779., 27549., 29660., 23356.])

训练模型

# 拟合 stepwise auto-ARIMA

stepwise_fit = pm.auto_arima(

y = wineind,

start_p = 1,

start_q = 1,

max_p = 3,

max_q = 3,

seasonal = True,

d = 1,

D = 1,

trace = True,

error_action = "ignore",

suppress_warnings = True, # 收敛信息

stepwise = True,

)

Performing stepwise search to minimize aic

ARIMA(1,1,1)(0,0,0)[0] intercept : AIC=3508.854, Time=0.17 sec

ARIMA(0,1,0)(0,0,0)[0] intercept : AIC=3587.776, Time=0.01 sec

ARIMA(1,1,0)(0,0,0)[0] intercept : AIC=3573.940, Time=0.01 sec

ARIMA(0,1,1)(0,0,0)[0] intercept : AIC=3509.903, Time=0.06 sec

ARIMA(0,1,0)(0,0,0)[0] : AIC=3585.787, Time=0.00 sec

ARIMA(2,1,1)(0,0,0)[0] intercept : AIC=3500.610, Time=0.09 sec

ARIMA(2,1,0)(0,0,0)[0] intercept : AIC=3540.400, Time=0.02 sec

ARIMA(3,1,1)(0,0,0)[0] intercept : AIC=3502.598, Time=0.14 sec

ARIMA(2,1,2)(0,0,0)[0] intercept : AIC=3503.442, Time=0.15 sec

ARIMA(1,1,2)(0,0,0)[0] intercept : AIC=3505.978, Time=0.19 sec

ARIMA(3,1,0)(0,0,0)[0] intercept : AIC=3516.118, Time=0.04 sec

ARIMA(3,1,2)(0,0,0)[0] intercept : AIC=3504.888, Time=0.10 sec

ARIMA(2,1,1)(0,0,0)[0] : AIC=3500.251, Time=0.04 sec

ARIMA(1,1,1)(0,0,0)[0] : AIC=3509.015, Time=0.04 sec

ARIMA(2,1,0)(0,0,0)[0] : AIC=3538.500, Time=0.02 sec

ARIMA(3,1,1)(0,0,0)[0] : AIC=3502.238, Time=0.09 sec

ARIMA(2,1,2)(0,0,0)[0] : AIC=3503.042, Time=0.10 sec

ARIMA(1,1,0)(0,0,0)[0] : AIC=3571.973, Time=0.01 sec

ARIMA(1,1,2)(0,0,0)[0] : AIC=3508.438, Time=0.05 sec

ARIMA(3,1,0)(0,0,0)[0] : AIC=3514.328, Time=0.03 sec

ARIMA(3,1,2)(0,0,0)[0] : AIC=3504.226, Time=0.12 sec

Best model: ARIMA(2,1,1)(0,0,0)[0]

Total fit time: 1.478 seconds

查看模型信息

开发环境信息:

print(pm.show_versions())

System:

python: 3.7.10 (default, Mar 6 2021, 16:49:05) [Clang 12.0.0 (clang-1200.0.32.29)]

executable: /Users/zfwang/.pyenv/versions/3.7.10/envs/ts/bin/python

machine: Darwin-22.1.0-x86_64-i386-64bit

Python dependencies:

pip: 22.2.2

setuptools: 47.1.0

sklearn: 1.0.2

statsmodels: 0.13.2

numpy: 1.21.6

scipy: 1.7.3

Cython: 0.29.30

pandas: 1.3.5

joblib: 1.1.0

pmdarima: 1.8.5

模型信息:

print(stepwise_fit.summary())

SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 176

Model: SARIMAX(2, 1, 1) Log Likelihood -1746.125

Date: Sun, 13 Nov 2022 AIC 3500.251

Time: 00:19:45 BIC 3512.910

Sample: 0 HQIC 3505.386

- 176

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.1420 0.109 1.307 0.191 -0.071 0.355

ar.L2 -0.2572 0.125 -2.063 0.039 -0.502 -0.013

ma.L1 -0.9074 0.052 -17.526 0.000 -1.009 -0.806

sigma2 2.912e+07 1.19e-09 2.44e+16 0.000 2.91e+07 2.91e+07

===================================================================================

Ljung-Box (L1) (Q): 0.01 Jarque-Bera (JB): 0.48

Prob(Q): 0.92 Prob(JB): 0.79

Heteroskedasticity (H): 1.37 Skew: -0.12

Prob(H) (two-sided): 0.23 Kurtosis: 2.92

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[2] Covariance matrix is singular or near-singular, with condition number 2.74e+32. Standard errors may be unstable.

序列化模型

pickle

import pickle

# pickle serialize model

with open("arima.pkl", "wb") as pkl:

pickle.dump(stepwise_fit, pkl)

# pickle load model

with open("arima.pkl", "rb") as pkl:

pickle_preds = pickle.load(pkl).predict(n_periods = 5)

joblib

import joblib

# joblib serialize model

with open("arima.pkl", "wb") as pkl:

joblib.dump(stepwise_fit, pkl)

# joblib load model

with open("arima.pkl", "rb") as pkl:

joblib_preds = joblib.load(pkl).predict(n_periods = 5)

对比 pickle 和 joblib 结果

np.allclose(pickle_preds, joblib_preds)

使用新的观测样本更新模型

# data

wineind = load_wineind().astype(np.float64)

train, test = wineind[:125], wineind[125:]

# 拟合 stepwise auto-ARIMA

stepwise_fit = pm.auto_arima(

y = wineind,

start_p = 1,

max_p = 3,

start_q = 1,

max_q = 3,

seasonal = True,

d = 1,

D = 1,

trace = True,

error_action = "ignore",

suppress_warnings = True, # 收敛信息

stepwise = True,

)

# ARIMA model

arima = pm.ARIMA(order = (2, 1, 1), seasonal_order = (0, 0, 0, 0))

arima.fit(train)

# pickle serialize model

with open("arima.pkl", "wb") as pkl:

pickle.dump(arima, pkl)

# pickle load model

with open("arima.pkl", "rb") as pkl:

arima = pickle.load(pkl)

pickle_preds = arima.predict(n_periods = 5)

# 更新模型

arima.update(test)

# pickle serialize model

with open("arima.pkl", "wb") as pkl:

pickle.dump(arima, pkl)

auto_arima 使用

auto_arima 函数根据提供的信息准则(AIC、AICc、BIC 或 HQIC)将最佳 ARIMA 模型拟合到单变量时间序列。

该函数在提供的约束范围内对可能的模型和季节性阶数(seasonal orders) 执行搜索(逐步或并行),并选择最小化给定指标的参数

auto_arima 函数有很多参数需要调整,模型拟合的结果在很大程度上取决于其中的一些参数

了解 p, d 和 q

p:自回归模型(auto-regressive, AR)的阶数(order),即滞后观测值的数量- The order of the auto-regressive (AR) model (i.e., the number of lag observations). A time series is considered AR when previous values in the time series are very predictive of later values. An AR process will show a very gradual decrease in the ACF plot.

d:差分的自由度- The degree of differencing.

q:移动平均模型(moving average, MA)的阶数- The order of the moving average (MA) model. This is essentially the size of the “window” function over your time series data. An MA process is a linear combination of past errors.

ARIMA 模型的一般形式为 ,参数 和 可以用函数 auto_arima 进行迭代搜索,

但差分项 需要一组特殊的平稳性测试来估计

差分项 d

差分计算:

import pmdarima as pm

from pmdarima.utils import c, diff

# lag 1, diff 1

x = pm.c(10, 4, 2, 9, 34)

diff(x, lag = 1, differences = 1)

平稳性检验

自相关图:

import pmdarima as pm

from pmdarima import datasets

y = datasets.load_lynx()

pm.plot_acf(y)

ADFTest:

from pmdarima.arima.stationarity import ADFTest

adf_test = ADFTest(alpha = 0.05)

p_val, should_diff = adf_test.should_diff(y) # (0.01, False)

PPTest:

KPSSTest:

的估计:

from pmdarima.arima.utils import ndiffs

# ADF test

n_adf = ndiffs(y, test = "adf")

# KPSS test

n_kpss = ndiffs(y, test = "kpss")

# PP test

n_pp = ndiffs(y, test = "pp")

assert n_adf == n_kpss == n_pp == 0

在 ARIMA 模型的情况下,使数据平稳的最简单方法是允许 auto_arima 发挥其魔力,估计适当的 d 值,

并相应地区分时间序列。然而,其他用于强制平稳性的常见转换包括(有时相互结合):

- 平方根或 N 次根变换

- 去趋势化

- 对时间序列进行一次或多次差分

- 对数转换

了解 P, Q, D 和 m

季节性 ARIMA 模型有三个类似于 p, d, d 的参数:

P:自回归 (AR) 模型的季节性成分的阶数D:季节性过程的差分阶Q:移动平均 (MA) 模型的季节性成分的阶数

P 和 Q 的估计类似于通过 auto_arima 模型估计 p、q,而 D 的估计可以通过 Canova-Hansen 检验,

季节性差分项 D 的估计

默认情况下,如果在 auto_arima 中设置 seasonal=True,D 会被估计,但是要设置好 m 和 max_D

from pmdarima.datasets import load_lynx

from pmdarima.arima.utils import nsdiffs

# data

lynx = load_lynx()

# Canova-Hansen test

D = nsdiffs(

lynx,

m = 10,

max_D = 12,

test = "ch",

)

# OCSB test

nsdiffs(

lynx,

m = 10,

max_D = 12,

test = "ocsb"

)

设置 m

m 参数与每个季节周期的观察次数有关,并且是一个必须先验已知的参数。

通常,m 将对应于一些经常性的周期性,例如:

- 7 - daily

- 12 - monthly

- 52 - weekly

import pmdarima as pm

# data

data = pm.datasets.load_wineind()

train, test = data[:150], data[150:]

# model

m1 = pm.auto_arima(

train,

error_action = "ignore",

seasonal = True,

m = 1

)

m12 = pm.auto_arima(

train,

error_action = "ignore",

seasonal = True,

m = 12

)

并行和逐步

auto_arima 函数有两种模式:

- stepwise

- parallelized(比较慢)

基本步骤:

- 尝试从四个可能得模型开始

ARIMA(2, d, 2)ifm=1andARIMA(2, d, 2)(1, D, 1)ifm>1ARIMA(0, d, 0)ifm=1andARIMA(0, d, 0)(0, D, 0)ifm>1ARIMA(1, d, 0)ifm=1andARIMA(1, d, 0)(1, D, 0)ifm>1ARIMA(0, d, 1)ifm=1andARIMA(0, d, 1)(0, D, 1)ifm>1

- 考虑其他的模型

- Where one of p, q, P and Q is allowed to vary by ±1 from the current best model

- Where p and q both vary by ±1 from the current best model

- Where P and Q both vary by ±1 from the current best model

StepwiseContext

import pmdarima as pm

from pmdarima.arima import StepwiseContext

# data

data = pm.datasets.load_wineind()

train, test = data[:150], data[150:]

# model

with StepwiseContext(max_dur = 15):

model = pm.auto_arima(

train,

stepwise = True,

error_action = "ignore",

seasonal = True,

m = 12

)

Pipeline

可以应用的模型:

ARIMAAutoARIMA

import pmdarima as pm

from pmdarima.pipeline import Pipeline

from pmdarima.preprocessing import BoxCoxEndogTransformer

# data

wineind = pm.datasets.load_wineind()

train, test = wineind[:150], wineind[150:]

# pipeline

pipeline = Pipeline([

("boxcox", BoxCoxEndogTransformer()),

("model", pm.AutoARIMA(seasonal = True, suppress_warnings = True))

])

# model fit

pipeline.fit(train)

# model predict

pipeline.predict(n_periods = 5)